- Tags: Building A Home, Design, First Home Buyers, First National News, Gold Coast Property, How To, Landlords, Law, News, Property Investment, Real Estate, Selling Property, Tax, Top Read

Depreciation Deductions You’ll Flip For!

Changed legislation benefits renovators

Renovating or ‘property flipping’ has become a huge trend in Australia, especially on the eastern seaboard where according to CoreLogic almost 7 per cent of transactions in Sydney, Melbourne and Brisbane were sold shortly after purchase following a renovation.

CoreLogic’s data also demonstrates that 90 per cent of properties flipped during 2017 were sold for a profit.

‘Property flipping’ occurs when an investor buys, renovates and resells a property within a relatively short space of time, with the intention of making a profit.

Legislation passed through the Senate on the 15th of November 2017 has changed the way depreciation for pre-existing plant and equipment found in second-hand properties will be treated.

Plant and equipment depreciation covers all removable and mechanical assets which generally depreciate faster than the building.

The legislation states that investors who purchase second-hand residential properties after 7:30pm on the 9th of May 2017 cannot claim depreciation on pre-existing plant and equipment unless the property is deemed to have been substantially renovated or is brand new.

Below are some examples of structural and non-structural works, that in combination could be considered substantial when property flipping:

- Structural: altering, removing or replacing foundations, floors, supporting walls or part thereof (interior or exterior), lifting or modifying roofs, replacing existing windows or doors where brickwork is altered (single to double door)

- Non-structural: replacing electrical wiring or plumbing, replacing, removing or altering non-supporting walls

So, if a property is considered to be substantially renovated before it is sold, then the plant and equipment depreciation can be claimed on all the removable and mechanical assets by the new owner.

Capital works deductions on the structure of a building including any fixed and irremovable assets were not affected by the new legislation and generally make up 85 to 90 per cent of the total claimable amount. Current investors can continue to claim these deductions for both existing and new additions, regardless of when the work took place.

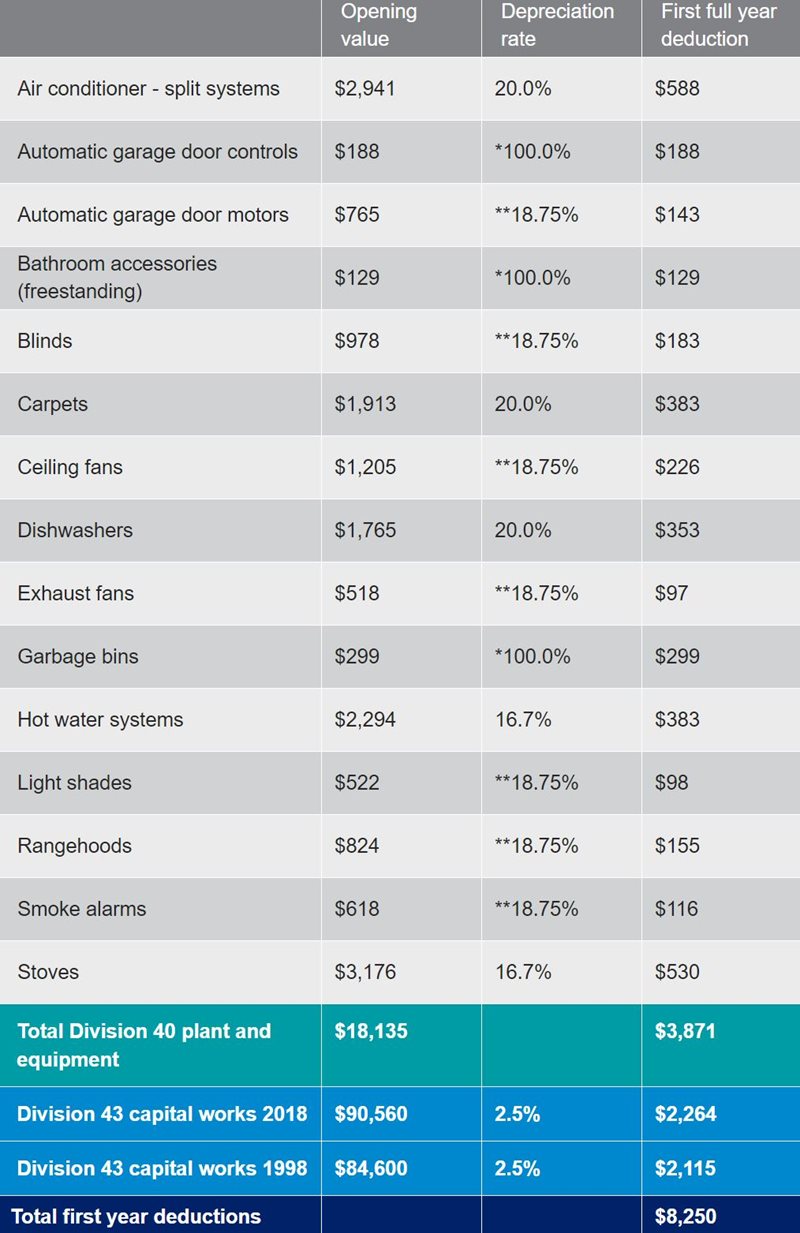

To demonstrate, we looked at an example of a second-hand property built in 1973 that an investor recently purchased.

The property had recently undergone a renovation. Due to the extent of the renovation, BMT Tax Depreciation could assess the property as substantially renovated, allowing the new owner to claim depreciation for all the plant and equipment and new capital works.

In addition, during their inspection BMT identified that a small extension had taken place in 1998. Because capital works deductions are unaffected by the legislation change, the current owners were able to claim it for this renovation even though it was completed twenty years ago by previous owners.

The table below demonstrates the deductions this particular client could claim for plant and equipment depreciation and capital works.

Renovation Example

Assumptions and disclaimer

Assumptions and disclaimer:

The depreciation deductions in this example have been calculated using the diminishing value method. *An immediate write-off has been applied to assets with an opening value of less than $300. **Low-value pooling has been applied to assets valued less than $1,000. These items will depreciate at a rate of 18.75% in the first financial year and 37.5% from the second year onwards.

As the table shows, BMT identified $8,250 in both capital works and depreciation deductions for the new owner of this property.

Investors who renovate a rental property they own must note that they are likely removing structures or assets that have a remaining un-deducted value. This can be claimed as a deduction in full when the asset is removed.

A specialist Quantity Surveyor, such as BMT Tax Depreciation, should be engaged prior to work starting to make sure that all removed items are identified and captured within a depreciation schedule.

Investors who are considering purchasing any property can request a free tax depreciation estimate.

SOURCE: BMT QUANTITY SURVEYORS - MAVERICK - TAX DEPRECIATION

by BMT Quantity Surveyors

Depreciation Deductions You’ll Flip For!

palmbeachfn.com.au August 2018 First National Palm Beach Cnr of 6th Ave & Cypress Terrace, Palm Beach, QLD 4221

Ph: 07 5559 9600